Tag: milk prices

DMC Margin Posts Another Sizeable Drop in February

The Dairy Margin Coverage (DMC) program will pay $3.31/cwt for $9.50/cwt coverage in February, based on a margin of $6.19/cwt that month. This was $4.70/cwt less than the margin last November. A milk price drop of $1.50/cwt from a month earlier and a $0.25/cwt rise in the DMC feed cost formula combined to lower the February margin by $1.75/cwt from its level in January.

Available forecasts currently indicate that the monthly DMC margins are close to bottoming out for the year, at around $6.00/cwt in a month or two, followed by a slow rise that will not likely top $9.50/cwt until the fourth quarter. This year will return many times the cost of this very affordable means of managing margin risk.

Exports Stoke Dairy Demand as Inflation Bites U.S. Consumption

Record Exports Show Dairy’s Global Reach; Cheese Demand Rises

Exports Buoy Dairy as Inflation Erodes Domestic Demand

Falling Prices, Rising Opportunities on Tap for 2023

Record milk prices seen in 2022 likely won’t repeat themselves, as production increases and consumers grapple with an economic slowdown, according to members of the NMPF and U.S. Dairy Export Council’s joint economics unit, in a Dairy Defined Podcast released today. But exports are on track to increase, and demand will likely be resilient as dairy remains must-have for buyers.

“Consumers around the world still gravitate towards dairy, even when they’re experiencing tighter economic situations,” said Will Loux, head of the team Vice President for Global Economic Affairs with NMPF and USDEC. “They ultimately view dairy as an essential item and will continue to consume it.”

Loux discusses the global and domestic dairy outlook with NMPF’s Chief Economist, Peter Vitaliano; Economic Research and Analysis Director, Stephen Cain; and the joint economic team’s newest member, Economic Policy and Global Analysis Coordinator, Allison Wilton. The full podcast is here. You can also find the podcast on Apple Podcasts, Spotify and Google Podcasts. Broadcast outlets may use the MP3 file below. Please attribute information to NMPF.

Rising Domestic Use Supports Prices

No DMC payments for October as Prices Rise

The U.S. average all-milk price rose $1.50/cwt in October from a month earlier, boosting the month’s DMC margin well above the $9.50/cwt maximum coverage level needed to trigger program payments, after two months of payouts.

The October margin was $10.71/cwt, $2.09/cwt higher than September’s margin. The DMC feed cost dropped by $0.59/cwt in October, driven entirely by a sizeable drop in the price of corn.

Another small payment for $9.50/cwt Tier 1 coverage may be triggered in December, based on current projects. Payments this year under the program, for August and September, together total the equivalent of about $0.19/cwt on an annualized basis and would be enough to cover the annual premium for a farmer enrolled in DMC at the $9.50 coverage level.

NMPF’s Galen on DMC Signup

NMPF Senior Vice President Chris Galen reminds farmers of the upcoming Dec. 9 deadline to enroll in the Dairy Margin Coverage Program in an interview with the National Association of Farm Broadcasters. This year’s payments under the program — the result of high input costs eating into record prices — show the wisdom of DMC’s design, Galen said. “As we head into 2023, we know that milk prices aren’t going to be as strong,” Galen said. “We know that input costs are still going to be significant.”

Cheese Sales Drive U.S. Dairy Consumption Growth

China’s Dairy Demand May Be Sluggish in ’23

By Stephen Cain, Director of Research and Economic Analysis, NMPF.

Outside of cheese, China is the number one importer of essentially every major dairy product. Globally, the world’s most populated country purchases 27% of all traded dairy products on a milk solids basis. China accounts for roughly 20% of all U.S. dairy exports and nearly half of all U.S. dry whey exports.

Outside of cheese, China is the number one importer of essentially every major dairy product. Globally, the world’s most populated country purchases 27% of all traded dairy products on a milk solids basis. China accounts for roughly 20% of all U.S. dairy exports and nearly half of all U.S. dry whey exports.

All of this makes China an unquestionably important market; yet, over the last year, Chinese demand has been down significantly. Chinese milk solids imports over the last 12 months are down 16%, and they’re heavily down in skim milk powder (-20%), dry whey (-17%), and whole milk powder (-24%). Two key pieces that have led to the pullback are high stockpiles and COVID-19 lockdowns.

Following the onset of the pandemic and wanting to ensure adequate supplies on hand, China built up some impressive stocks, especially in skim milk power and dry whey. From mid-2020 through mid-2021, Chinese milk solids imports climbed 32% over the preceding 12 months. For the same time period, skim milk powder and dry whey imports rose 32% and 50%, respectively.

This high purchase volume outpaced demand and led to stock build up. These high stocks, coupled with then-high global prices, led China to pull back from the global market and instead work down its stockpiles. That largely kept Chinese purchasing depressed over the past year. Encouragingly, stocks are now approaching more normal levels, which supports China returning to the market, especially for skim milk powder and dry whey.

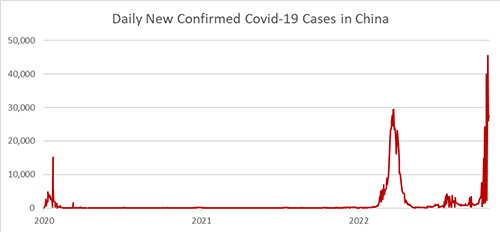

More COVID-19 lockdowns throughout China are also plaguing demand. While the rest of the world moves on from the pandemic and reverts to pre-COVID-19 life, China seems to be charging in the opposite direction. The zero-COVID policy in China has led to extreme measures in the country, with huge swaths of the population being locked down as the country continues its losing battle against the disease.

Earlier this year, Shanghai, the largest city in China with roughly 25 million residents, was put in lockdown for two consecutive months. Since then, lockdowns have only increased in number and severity, with some estimates as of late October stating there were more than 200 million people affected by lockdowns nationwide.

While many agree China relaxing its zero-COVID approach would be beneficial, rising cases in the country suggest that’s unlikely to occur. The country is facing the highest rate of new cases since the start of the pandemic, which means lockdowns and tough restrictions are only going to become more commonplace. That’s hitting dairy demand. Restaurants and the food service sector are hugely important to dairy consumption in China, but that consumption avenue is being restricted as consumers are increasingly unable to leave their homes. Until lockdowns and restrictions ease, Chinese dairy demand will continue to be challenged.

Source: USDEC, Our World in Data

Dairy is only one part of a Chinese economy that’s facing headwinds. A limited gross domestic product (GDP) growth outlook, a teetering real estate sector, and depressed, COVID-19-driven demand from lockdowns are creating a challenged economic outlook. The 2022 GDP forecast is estimated at 3.2%, which would make for one of the worst performances in nearly half a century; 2023 looks only slightly better, with forecast growth of around 4.4%.

Similarly, Chinese dairy demand in 2023 is likely to see similar sluggish growth. Despite the melancholy economic outlook and lockdown projections, Chinese imports in 2023 will likely be up, but not at substantial volumes, and certainly not same at the growth rate we saw in 2021. As stocks are depleted and domestically produced products (which are largely more expensive than imports) fail to meet demand, China will have to return to the global market. The biggest swing factor, though, remains COVID-19 lockdowns. If China doubles down on lockdowns, demand will likely continue to be depressed and imports will be challenged. Should they ease, China will certainly need product, and greater imports will follow — and that would be good news for U.S. exporters.

This column originally appeared in Hoard’s Dairyman Intel on Nov. 28, 2022.

NMPF’s Bjerga on the Congressional Elections and Dairy’s Challenges

NMPF Senior Vice President of Communications Alan Bjerga details some of the policy and marketplace challenges U.S. dairy is striving to meet, regardless of the cloudy outcomes of Tuesday’s congressional elections, in an interview with RFD-TV. Opportunities to grow markets via sustainability, an adequate safety net in the upcoming farm bill, and sensible industry regulation all loom in 2023, with dairy well-positioned to make progress.