Randy Mooney, a dairy farmer from Rogersville, MO and for 17 years the chariman of the National Milk Producers Federation, reflects on his tenure shortly after stepping down from the role at the organization’s annual meeting. Mooney, who remains on NMPF’s executive board, discusses dairy’s bright future and the honor of serving dairy in an interview with RFD-TV.

Tag: dairy economics

Rollins Touts Milk Action Plan at Annual Meeting

ARLINGTON, TX – Agriculture Secretary Brooke Rollins touted the Trump administration’s milk action plan to support American dairy farmers today at NMPF’s annual meeting.

“I want to be very clear. We will never stop fighting for those of you in the dairy industry and across rural America we have reached that golden age for our producers,” said Rollins, a Texas native who keynoted the Joint Annual Meeting hosted by NMPF, the United Dairy Board and the United Dairy Industry Association. “Dairy farmers have delivered for America for 250 years, and now it’s time for us to deliver for you.”

Rollins spoke to roughly 750 farmers, cooperative leaders and industry professionals gathered to discuss industry topics ranging from an economic outlook to dairy labor challenges. NMPF, the largest U.S. dairy farmer group, is holding a series of discussions on policy issues throughout the meeting, ranging from the need to pass the Whole Milk for Healthy Kids Act to creating lasting labor solutions for U.S. dairy farmers.

In her remarks, Rollins outlined USDA’s dairy priorities, outlining the administration’s four-point approach to support the industry, including:

- Incentivizing dairy consumption through changes to the Dietary Guidelines for Americans, expected in December or early January;

- Working to drive down input costs;

- Facilitating investments in American milk processing; and

- Expanding markets to help milk producers prosper.

Rollins also noted the importance of farm-labor issues, pledging to seek federal changes to rules and regulations in coordination with the departments of Labor and Homeland Security while noting that broader changes will require congressional action. “We are acutely aware of the unique labor needs of the dairy industry,” she said.

Rollins became the 33rd U.S. Secretary of Agriculture earlier this year after serving as the Founder, President, and Chief Executive Officer of the America First Policy Institute. During President Trump’s first administration, she was the Director of the Domestic Policy Council and Assistant to the President for Strategic Initiatives in the White House. She also previously served as Director of the Office of American Innovation. In these roles, she developed and managed the domestic policy agenda of the Trump administration.

Rollins’s remarks kicked off a busy day at the conference, with remarks from immediate past NMPF Chairman Randy Mooney, newly elected NMPF Chairman Brian Rexing, and NMPF President & CEO Gregg Doud as well as a luncheon featuring awards from the National Dairy Farmers Assuring Responsible Management (FARM) Program and NMPF communications.

A reception sampling top-performing cheeses from NMPF’s annual cheese contest is this evening.

Dairy’s Future Bright, IDFA, NMPF Chairmen Say

Dairy’s future is bright, and it’s brightest when the industry is united toward common goals, the chairmen of the International Dairy Foods Association and the National Milk Producers Federation said.

“$11 billion or so in projects are happening or about to happen that will significantly grow the industry capacity throughout the country,” said Daragh Maccabee, CEO of Idaho Milk Products and Chairman of the International Dairy Foods Association (IDFA) in the podcast released today. “That means the processor community is stepping up, and we all know that the dairy producer community will do its part as dairy farmers always, always do. And aligned with that investment also comes furthering innovation capabilities or further investment in innovation capabilities so that the U.S. can continue to lead the way in delivering value for milk in increasingly sophisticated ways.”

The discussion covers the unique qualities of the U.S. dairy industry, including its scale, efficiency, and sustainability. Maccabee and Mooney, who serves as chairman of the National Milk Producers Federation and Dairy Farmers of America, the largest U.S. dairy co-op, with the strength of cooperatives and industry organizations are also highlighted as keys to industry progress. However, dairy faces challenges around labor shortages and trade uncertainty, they said.

“We need new laws that help farmers continue to have the labor that we need on the farms to produce the milk. And without that, that’s the biggest critical issue that I see as what could affect future dairy production in this country, is just making sure the cows get taken care of and the cows get milked under the labor standards that we have today,” Mooney said.

Still, the industry’s overall outlook remains something to cheer about, said Mooney, who soon will be stepping down as NMPF’s chairman. Reflecting on nearly two decades of leadership in that role, Mooney said it’s been an honor to be part of a profession that improves people’s lives.

“This industry is going to be bright for the future of farming. It’s going to be bright for the producers,” he said. “And not only that, what makes me feel good at the end of the day is on our individual farms.”

To hear more Dairy Defined podcasts, you can find and subscribe to the podcast on Apple Podcasts, Spotify and Amazon Music under the podcast name “Dairy Defined.”

NMPF Staff Deliver Outlooks, Trade Messages

NMPF staff reached out across dairy and agriculture audiences in September and during the August congressional recess with appearances in local and national meetings, discussing dairy’s economic outlook and the importance of free trade.

NMPF’s Jaime Castaneda, executive vice president for policy development and strategy, provided agricultural trade leaders and government officials a snapshot of opportunities and challenges for U.S. dairy exports in an unprecedented trade environment as a panelist at this year’s Midwest Agricultural Export Summit on Aug.13.

Hosted by South Dakota Trade in Sioux Falls, the event convened producers, policymakers and trade professionals in a forum to equip farmers and ranchers with the tools necessary to compete and grow in international markets. Castaneda joined a panel, “Breaking Down Barriers: Agriculture Industry Perspectives,” to discuss existing barriers to dairy trade and the Trump Administration’s newly announced trade frameworks.

Meanwhile, economics team staff addressed market outlooks domestically and internationally.

Will Loux, head of the joint economics team for NMPF and the U.S. Dairy Export Council, traveled Sep. 8-12 to Sydney, Australia to explore the potential for NEXT and U.S. dairy products in that market.

NMPF Market Analyst Allison Wilton gave a market outlook to the American Association of Bovine Practitioners in Omaha at its annual conference on Sep. 11. Later in the month she gave a similar presentation to Darigold staff in Seattle.

Stephen Cain, Vice President of Economic Policy and Market Analysis, in September presented at the U.S. Dairy Ingredient Supply Seminar in Ho Chi Minh City, Vietnam, and to Bangkok, Thailand for the U.S. Dairy Supply & Innovation Seminar.

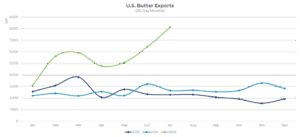

Butter exports shift in our favor

By Will Loux, Senior Vice President, Global Economic Affairs

By Will Loux, Senior Vice President, Global Economic Affairs

In an article earlier this year, I asked the question whether the U.S. could export its way out of the glut of cream that had filled the market. I posited that while it would take a while for U.S. exports to start growing in earnest due to the high cost of entry for first-time exporters, the market signals were such that the U.S. would inevitably need to sell more butterfat overseas.

As evidenced by June and July’s export data, that flow of butterfat to international markets has arrived in earnest. June was the U.S.’ largest month of butter exports since 2014, only to be bested just one month later. The U.S. even managed to sell over 2,000 metric tons (MT) of butter to the European Union in July, overcoming a normally cost-prohibitive tariff of 50 cents per pound. The U.S. is also exporting greater volumes of anhydrous milkfat than ever before. In fact, combined exports of butter and anhydrous milkfat (AMF) have grown by more than any other dairy product so far this year on a component-adjusted basis.

The question today is no longer whether the U.S. will export butterfat but rather how much, and can the U.S. become a consistent exporter moving forward?

From a short-term perspective, the path seems clear for the U.S. to sell more butterfat overseas. The U.S. remains highly competitive on price today despite European and New Zealand prices falling. Just as importantly, the U.S. still has plenty of supply available for export despite the surge in exports and solid domestic sales of butter. Simply, the exponential growth in U.S. milkfat tests combined with U.S. dairy herds in expansion mode means the U.S. should have allocation available at an affordable price for international customers for the foreseeable future. While making export spec butter is usually a special run for American manufacturers, U.S. exporters and international buyers are undoubtedly working to get U.S. butterfat products in variety of overseas markets.

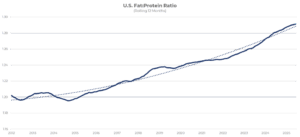

Even from a longer-term perspective, there are plenty of reasons to suggest the U.S. could be undergoing a paradigm shift in favor of greater export business for butter and AMF. The fat-to-protein ratio in milk continues to rise, meaning U.S. cheese manufacturers are now faced with more milkfat than required for cheesemaking. Additionally, the rise in ultra-filtered and protein-fortified beverages will also result more cream moving onto the market. Finally, and just as importantly, the recovery in global demand means international buyers are looking for suppliers besides New Zealand and Europe, the latter of whom have been retreating from commodity fat markets within the last several years.

The investment and strategic foresight to position the U.S. as a consistent player in global butterfat markets, will take plenty of time. However, it wouldn’t be the first time the U.S. dairy industry has identified an opportunity, embraced the challenge, and emerged stronger and more resilient for it.

This column originally appeared in Hoard’s Dairyman Intel on Sept. 15, 2025.

FMMO Modernization Takes Effect, With NEXT Next

- Final Rule updating Federal Milk Marketing Order pricing formulas implemented June 1

- NMPF Exports & Trade (NEXT) gained approval from NMPF’s Board of Directors and started accepting bids

NMPF’s Economics team saw the culmination of a multi-year effort to update the Federal Milk Marketing Order pricing formulas on June 1, when the new FMMO rule took effect.

The “higher-of” Class I price mover for most non-ESL milk has been restored; dairy product make allowances and Class I differentials nationwide are updated, and USDA is no longer using barrel cheese to determine the Class III price. USDA will implement a final part of the rule increasing the component composition factors for skim milk in all FMMO price classes Dec. 1 to avoid disrupting existing risk management positions.

NMPF successfully argued for these necessary updates in five specific proposals presented at a record-long FMMO hearing from late summer 2023 to early winter 2024. The arguments all flowed from the fundamental principle that FMMO product price formulas must evolve with the changing structure of the dairy industry to properly fulfill their role of accurately translating dairy product prices into milk values embodied in the orders’ classified prices. The rule comes after more than four years of effort that included more than 200 meetings to formulate and defend NMPF’s proposal, led by NMPF leaders and experts.

Also spearheaded by economic analysis and consultations, NMPF’s Board of Directors approved the NMPF Exports & Trade (NEXT) program to succeed the Cooperatives Working Together export assistance program, at its June board meeting, with bids beginning in July.

NEXT expands its service to dairy producers and to testing innovative new ways to expand U.S. dairy’s market share. NEXT provides an effective means to move domestic dairy products to overseas markets by helping to overcome U.S. dairy’s trade disadvantages. New initiatives in the new NEXT program include:

- Expanding the program’s product mix

- Creating market development initiatives that provide targeted, additional support beyond primary assistance to level the playing field and drive U.S. export volume growth in key markets around the world where the U.S. is at a tariff

disadvantage and/or where the U.S. has the room and ability to gain market share - Enhancing program operations to assist in NEXT’s mission by extending delivery periods, removing volume limits and providing greater insight into program operations; and

- Creating a strategic advisory council to guide program strategy.

NEXT charges cooperatives paying into the new program two cents/cwt of member milk, a reduction from the four cents/cwt previous assessment in the CWT program. Within the first month of the program, NEXT-assisted export sales boomed, reaching nearly 38 million pounds of product – a tremendous start for the new program.

Dairy Exports Surge in June, Dairy Product Stocks Hold Steady

June DMC Margin Rises $0.70/cwt

The June margin for the Dairy Margin Coverage Program was $11.10/cwt in June, an increase of $0.70/cwt from May. The June all-milk price was unchanged from May at $21.30/cwt, while the June DMC feed cost formula dropped by $0.70/cwt for the month, as the prices of all three formula feed components decreased, particularly that for premium alfalfa hay.

The forecasts maintained by DMC Decision Tool on the USDA website at the end of July showed the DMC margin topping out $13.20/cwt in November and averaging $12.11/cwt for the year.

Dairy Maintains Momentum Through Turbulence

It doesn’t really need to be said, because evidence is everywhere. But it’s worth repeating, in light of how easy it is to lose focus among turbulence in labor, trade and politics: Dairy’s future is incredibly bright.

Any skepticism toward that idea can quickly be countered with about 10 billion reasons. That’s the dollar amount of investments in new dairy processing capacity that’s coming online between 2023 and 2026, according to an NMPF analysis. Ultimately, these investments are an investment in the U.S. dairy farmer.

From Washington state to Georgia, manufacturers are placing their bets on increased consumer demand for dairy products. State-of-the-art facilities are promising to put affordable, nutritious dairy foods on store shelves and dinner plates in the United States and around the world. The processing growth is creating new outlets for dairy farm production, a tide that lifts all boats across the industry.

And the realization that growing consumer demand isn’t just a forecast: It’s current reality.

- U.S. fluid-milk consumption rose last year for the first time since 2009. Milk’s market share versus plant-based imposters continues to rise (as if nut drinks were ever truly a threat in the first place).

- Cottage cheese has emerged as the go-to snack food for Generation Z.

- And per capita overall U.S. dairy demand continues at levels last seen in the 1950s.

All that is a tribute to the fact that, even with all the diet diversification since then, dairy remains a bedrock of American diets, accessible to all, affordable, and trusted. It’s also a tribute to the industry’s vision and how long-term producer investment in the dairy checkoff has encouraged innovation in new research, technologies, and products.

Overseas sales remain a bright spot for the industry as well. That may seem surprising, given all the headlines of volatility in global trade as the United States tries to reset global commerce. But it’s true: In 2025 through May, the value of U.S. dairy exports was $3.873 billion, 13% higher than the same period last year, when they were $3.422 billion.

That’s a powerful testament to the resilience of U.S. dairy producers and exporters who work around the clock, managing and building relationships that are being heavily tested this year. While overall year-to-date sales volumes are slightly down, and Chinese retaliatory tariffs have heavily weighed down sales to that market, higher-value products like high protein whey products have grown 8% by volume and 30% by value year-to-date. Similarly, U.S. cheese exports are up 7% by volume and 18% by value when compared to 2024 exports through May.

Recent progress in new trade deals with trade partners such as Indonesia also brings encouragement that eventually trade waters will calm, with new opportunities possible for U.S. dairy producers as the turbulence ebbs. Thank you, U.S. Dairy Export Council, thank you NMPF member cooperatives, thank you, NEXT Program, and most all thank you, dairy farmers, for keeping this momentum going.

All this, of course, isn’t meant to give short shrift to the significant challenges ahead. At NMPF we are well aware of the workforce challenges facing dairy farms as a nationwide crackdown on illegal immigration disrupts agricultural workforces. Current trade success so far doesn’t mean policy upheaval can’t damage or reverse progress, nor that export momentum will stay the same if new trade policies don’t improve global access opportunities. And consumer confidence faces misinformation threats that only become more sophisticated.

But heading into August, when Congress goes back home and policymaking hits a temporary pause, we at NMPF couldn’t be prouder to represent a growing, thriving industry — not one that’s free from challenges, but one that meets the challenges at hand. Dairy’s momentum becomes our momentum. That momentum is significant. It augurs well for the months and years to come.

Gregg Doud

President & CEO, NMPF

NMPF’s Castaneda Explains for Dairy Radio Now the Importance of Investigation of Milk Powder Trade

NMPF’s executive vice president Jaime Castaneda explains for listeners of Dairy Radio Now why NMPF asked the Trump Administration to investigate the world trade in milk powders, and, in particular, the impact of Canada’s protectionist practices on U.S. producers. Castaneda and NMPF colleague Will Loux testified this week on the issue.

U.S. Dairy Sees Strong Growth at Home Amid Challenging Trade Conditions

Little Change from April in May DMC Margin

The May DMC margin lost $0.02/cwt from a month earlier to $10.40/cwt, according to the DMC Decision Tool on the USDA Farm Service Agency website. The Tool had previously predicted the April margin to be the lowest for the year, but a large increase in the price of premium alfalfa hay, equivalent to $0.34/cwt of milk in the DMC feed cost formula, more than offset a $0.30/cwt increase in the May all-milk price, to $21.30/cwt, while much smaller, offsetting prices of corn and soybean meal could only bring the feed cost down by another $0.02/cwt.

The Decision Tool continues to show the DMC margin increasing steadily, now from May, to top out at $13.76/cwt in November and average $12.43/cwt for the year.