Hoard's Dairyman:

Protein demand pulling up milk checks

April 27, 2026

By Will Loux, Senior Vice President, Global Economic Affairs

By Will Loux, Senior Vice President, Global Economic Affairs

From its primacy in the latest dietary guidelines to front page headlines, protein is seemingly everywhere, and dairy is particularly well poised to supply the growing demand as the critical nutrient takes center stage in American diets. The good news for dairy producers is that the growing demand for dairy protein is starting to be reflected in their milk checks.

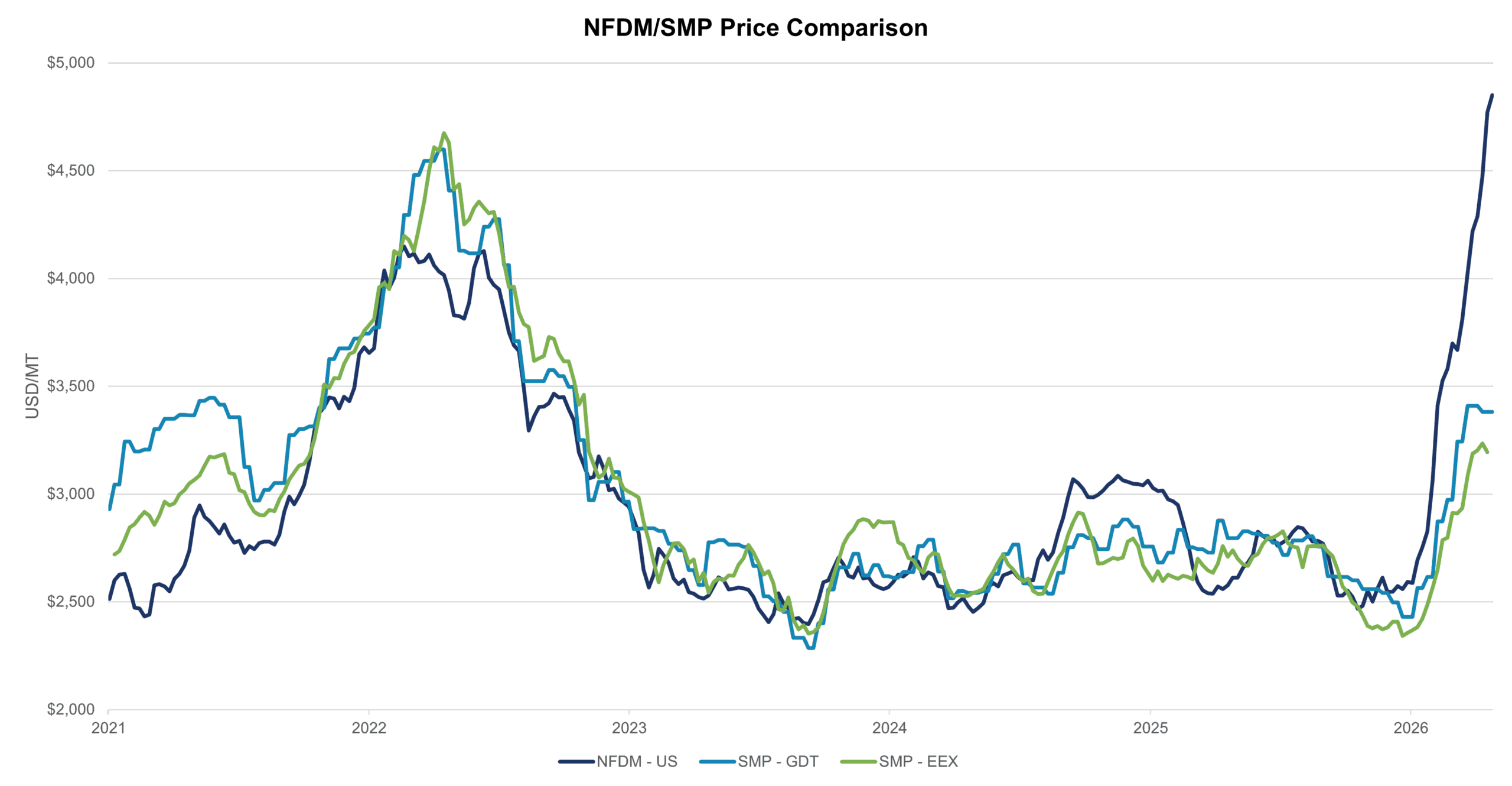

As nonfat dry milk (NFDM) prices hit record highs and dry whey prices sit comfortably above 60 cents, the positive sales momentum driven by today’s protein boom is directly translating into higher prices for dairy producers. In fact, the implied Class IV price based on CME spot values has improved by more than $10 per hundredweight (cwt.) since the start of the year, with most of the rally being driven by NFDM prices gaining by more than $1 per pound.

However, it isn’t specifically booming NFDM and dry whey demand that’s causing prices to rise. Rather, despite surging U.S. milk production, it is a lack of supply of those products that explains the improved prices. Simply put: Milk — and specifically protein — that otherwise would have gone toward sweet whey and nonfat dry milk is now being made into protein concentrates/isolates, ultrafiltered milk, and high-protein yogurts.

Taking a closer look at the numbers, in 2025, U.S. NFDM production was at its lowest ebb since 2013, while skim milk powder (SMP) fell to its lowest level since 2012. Even more startling, U.S. dry whey production was at its lowest for this century. Given U.S. skim solids production grew by 3.6% over the last 12 months, where is all that protein going?

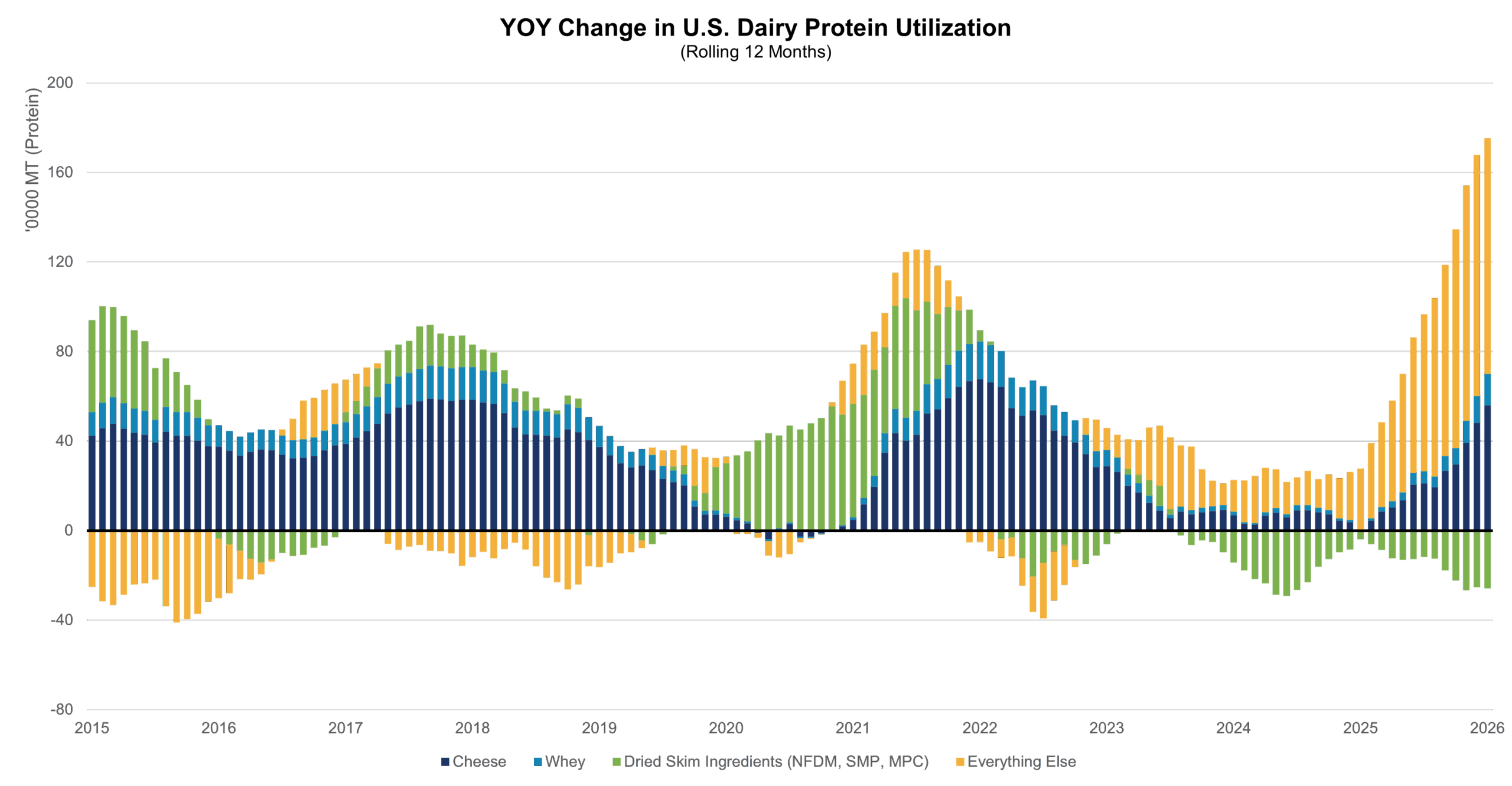

The chart above shows the year-over-year change of U.S. protein utilization by-product category on an annualized basis. Historically, cheese and whey were the primary users of dairy proteins (dark and light blue, respectively). The whey solids coming off the cheese vat are increasingly being directed toward whey protein concentrate 80 (WPC80) and whey protein isolate (WPI), where production is up a combined 10% on a protein-equivalent basis. Beyond cheese though, when milk outpaced cheese’s needs — due to either abundant supply or demand slowdowns such as the COVID-19 pandemic — milk historically went into balancing plants for manufacturing dried skim ingredients, like NFDM.

Today, however, the fastest-growing user of dairy protein is the “everything else” category in yellow, which is surging as U.S. yogurt and cottage cheese production grew by 388 and 31 million pounds, respectively, in 2025, demonstrating gains of 8% apiece. Production of protein-rich dairy beverages isn’t tracked by USDA, but all signs point to booming demand there as well.

In fact, the growth in production of these high-protein products absorbed the equivalent of 690 million pounds of SMP, or 32% of production. For producers, if that dairy protein had gone into the dryer, like it had in previous expansion cycles, it is difficult to imagine U.S. nonfat dry milk holding at $1.20 per pound, like it did for much of 2025, let alone rallying to today’s record highs.

Looking ahead, as favorable as protein demand is, $2.20 per pound for NFDM is likely unsustainable without international prices coming up to meet the United States. U.S. NFDM prices are 67 cents above SMP on the Global Dairy Trade (GDT) and 75 cents above European SMP. While 70% of U.S. NFDM and SMP production went toward either the domestic market or Mexico in 2025 (where the U.S. has a distinct freight and tariff advantage), and 665 million pounds went to highly contested markets, like Southeast Asia. If U.S. sales to these markets begin to ease, prices are likely to follow. Yet even if today’s altitude is unlikely to be maintained indefinitely, NFDM prices should be firmer than the last several years thanks to the strength and pull of protein in yogurts, cottage cheese, and beverages.

This column originally appeared in Hoard’s Dairyman Intel on April 27, 2026.